Accounting can vary widely based on industry, and nonprofit accounting is one of the most unique approaches to the subject. Instead of focusing on generating a profit for the organization, the core of nonprofit accounting is accountability toward supporters and toward the mission. Nonprofits track the amount of funding allocated to different programs, projects, and organizational operations to show stakeholders that they’re using all revenue to further the mission.

There are a few different financial statements central to nonprofit accounting. These statements help your organization with day-to-day financial management, are reviewed during audits, and store information in one place to make filing taxes easier.

In this article, we’ll walk through the three main financial statements your organization will use, as well as the top insights you can glean from each:

- Statement of Activities

- Statement of Financial Position

- Statement of Cash Flows

These three statements each have their own format and purpose, but they all help your organization make informed financial decisions. We recommend partnering with a nonprofit accountant to create and understand the financial statements in depth. For now, let’s dive into an overview of each statement’s function.

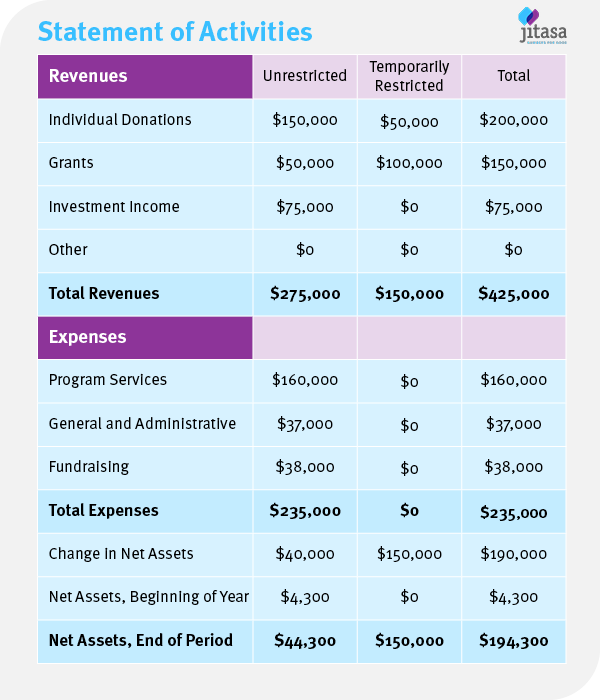

1. Statement of Activities

The statement of activities is the nonprofit equivalent of a for-profit income statement. It provides detailed information about your organization’s transactions and how those transactions were used to support your mission.

While filling out a statement of activities each year is required for nonprofits to comply with the generally accepted accounting principles (GAAP), it’s also helpful for your organization internally as it provides insights into where your funding comes from and how you’re using it.

What this statement includes

What this statement includes

The nonprofit statement of activities is broken down into three sections:

- Revenue. This section details your nonprofit’s funding sources and how much revenue you bring in from each source. 360MatchPro reports an increase in individual donations and corporate philanthropy in recent years—two common nonprofit revenue sources. Your organization may also bring in revenue from fundraising events, service fees, and grants.

- Expenses. This section shows all the costs your organization incurs, both operating and program expenses. The categories that operating expenses are divided into, such as employee salaries and fundraising event costs, will be similar across most organizations. However, program expenses can vary widely—an education-focused nonprofit may include the cost of books and supplies for after-school tutoring in their program expenses, while an animal shelter might incur dog grooming, training, and veterinary expenses.

- Net assets. You’ll determine your organization’s net assets by subtracting total expenses from total revenue. This section provides both your net assets of your total income as well as your assets of unrestricted funds. The second of these helps your organization better understand how much funding you actually have free for upcoming expenses.

One of the important aspects of this form is that it differentiates between restricted and unrestricted funding. Your nonprofit has to use restricted funds for a specific purpose, as opposed to unrestricted funds which can go toward any necessary expenses. Some funding is permanently restricted, while some is temporarily restricted and will become available to your organization after a project is completed or a period of time has elapsed.

Insights to glean from this statement

When you compare your nonprofit statement of activities with your budget, the line items in both the revenue and expenses sections should match up. So, the first insight that the statement of activities can show is whether your organization is on track to stick to your prepared budget for the year.

You can also use the statement of activities to determine whether your program expenses are sustainable long-term. The net assets section in particular can help you decide if you need to cut costs or add new revenue streams. Again, remember to review the section of your net assets that calculates assets without restrictions. If you fail to do this, you may think your revenue is sustainable if your net assets are positive, but restrictions might actually cause you to be in the red.

Finally, the statement of activities can help you fill out your tax forms. Form 990 requires nonprofits to report on revenue sources and expenses, which the statement of activities compiles in one place.

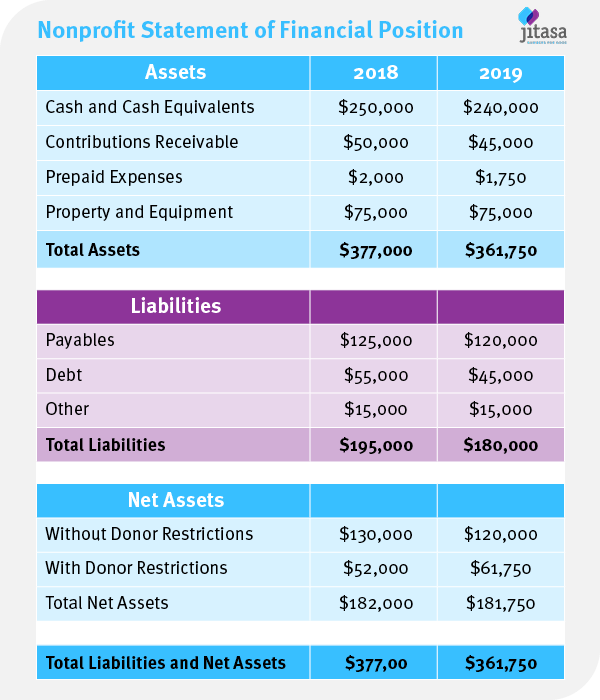

2. Statement of Financial Position

The nonprofit statement of financial position is also known as a balance sheet. Essentially, it shows a snapshot of your organization’s annual financial health by comparing assets and liabilities. When your nonprofit undergoes an audit, your balance sheet will play a key role in helping the auditor assess your organization’s internal controls and identify opportunities to improve your financial position.

What this statement includes

Like the statement of activities, the nonprofit statement of financial position has three sections:

- Assets. This section defines what your nonprofit owns, such as cash and cash equivalents, accounts receivable, prepaid expenses, and equipment. You’ll typically list these in order of liquidity. For example, cash goes at the top of the list because it’s already liquid, and equipment and property are listed near the bottom because you’d have to sell them for them to become liquid.

- Liabilities. This section explains what your nonprofit owes, like accounts payable, expenses charged by vendors or contractors, and debt incurred by your organization. These appear on the statement in order of due date, with short-term investments listed above long-term liabilities.

- Net assets. Similarly to the statement of activities, you’ll calculate the net assets on your balance sheet by subtracting liabilities from assets. These net assets are then separated into assets with donor restrictions, assets without restrictions, and total assets.

Accounting for restricted funds is also very important on the balance sheet so that you can see the assets you actually have available to conduct operations at your organization.

Insights to glean from this statement

The statement of financial position is a snapshot of your organization’s overall financial health because it shows how much flexibility you have to fund growth at your nonprofit. It’s also particularly useful in comparing data related to your nonprofit’s financial health across multiple years when you track these reports annually.

One major insight your balance sheet provides, though, is a measurement of your nonprofit’s current liquidity. Understanding your organization’s liquidity can help you determine whether your nonprofit is able to take on the financial risks associated with major projects by showing the amount of cash and assets you have available to cover extra expenses.

The most accurate way to determine your organization’s liquidity based on your statement of financial position is to calculate your months of liquid unrestricted net assets (LUNA) using this equation:

Months of LUNA = (Total Unrestricted Net Assets – Property and Equipment Assets) / Average Monthly Expenses

It’s generally recommended that your organization have three months of LUNA on hand to be considered financially stable. If you have less than three, you may need to readdress your financial position. But if you have more than three, you have enough financial flexibility to take some risks and pursue growth opportunities.

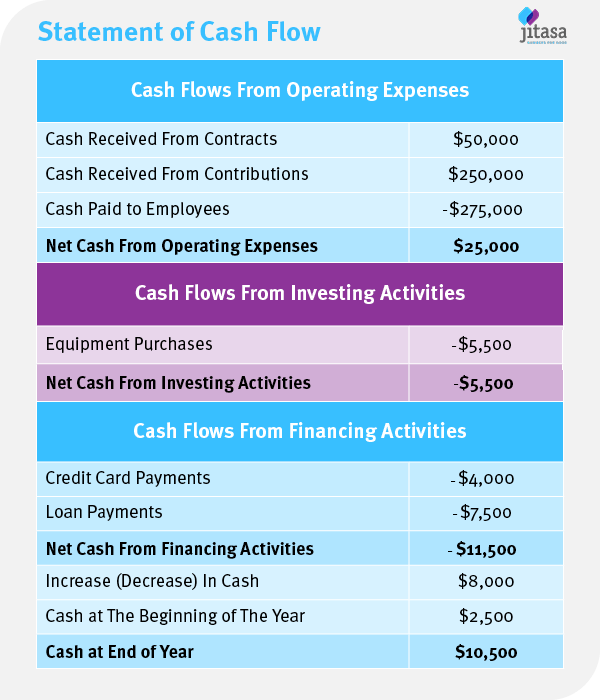

3. Statement of Cash Flows

The nonprofit statement of cash flows is just what it sounds like: a report showing how cash moves in and out of your organization. It differs from the other two statements in that it’s pulled on a monthly basis instead of annually.

What this statement includes

The statement of cash flows again has three sections, covering your nonprofit’s cash flows from:

- Operating expenses

- Investing activities

- Financing activities

Within each section, you’ll typically list each source of cash flow into your organization first as a positive number, and below that you’ll list cash outflows as negative numbers. This makes it easy to calculate your net cash for each section by adding all the inflows together and subtracting the total outflow.

Insights to glean from this statement

Knowing how much cash is flowing in and out of your organization helps you not only to develop a stronger fundraising plan, but also to evaluate your nonprofit’s spending habits. For example, if your statement shows that you brought in $10,000 from a fundraising event but spent $12,000 on programming, you’ll end up in the red and either need to cut expenses or find another funding source to make up the difference.

Jitasa’s guide to fund accounting points out that nonprofits need to appeal to supporters who want to understand where their donations go and how it helps the organization’s mission. Keeping a tight grip on where your funding goes from month to month will help you do just that.

Cash flow statements also help with effective nonprofit budgeting by showing the ways in which fundraising can vary throughout the year. You might notice, for instance, that the cash flow into your organization is always higher in November and December than in previous months because of the donations you receive on Giving Tuesday and during other year-end fundraising drives. So, you may decide to hold off on starting a new project until the end of the calendar year to make sure you have enough revenue to cover it.

The statements of activities, financial position, and cash flow each provide different insights in your nonprofit’s financial management and help maintain compliance in individual ways. When you review all three together, you’ll be able to determine whether your organization is on a path to sustainable financial growth.

I can’t wait to meet with you personally.

I can’t wait to meet with you personally.

Comments on this entry are closed.