Of the data your nonprofit collects, financial information is one of the most useful types—and one of the most complex to track. Keeping thorough, accurate records of your organization’s finances allows you to know how much funding you have on hand and effectively allocate it to further your mission. However, the wide range of revenue sources and expenses your nonprofit may have can quickly complicate your data collection and analysis.

To keep your financial data organized, you can use either of two primary tracking methods: cash accounting and accrual accounting. In this guide, we’ll discuss what each of these financial management systems looks like in practice, their respective benefits and drawbacks, and how to determine which method is right for your organization.

Cash Accounting Method

Cash accounting is the simpler of the two nonprofit accounting methods, so it’s most often used by smaller or newer organizations. Essentially, it tracks cash flow in and out of your nonprofit.

How It Works

In a cash accounting system, your nonprofit records revenue when it’s received and expenses when they’re paid. Even if you’ve promised to pay someone outside your organization for a service at a later date, or you know that funding from a donor or grantmaker is on the way to your nonprofit, you won’t officially recognize those transactions in your records until they’re completed. This distinction is particularly important when transactions span multiple fiscal years.

To see how this method works in practice, let’s say your nonprofit is planning its annual bikeathon fundraiser. The event is scheduled for this coming March, so you open registration in December to give participants plenty of time to sign up and collect pledges through their peer-to-peer fundraising pages. You also put down a deposit to rent folding tables and chairs and arrange to pay the outstanding balance when you pick up the supplies the day before the bikeathon.

Since the peer-to-peer donors won’t convert their pledges to donations until after the bikeathon, you’ll record all of those contributions under next year’s revenue totals if you’re using the cash accounting method. For the supply rental cost, you’ll consider the deposit as part of this year’s expenses and the payment of the outstanding balance as an expense for next year.

Benefits & Drawbacks of This Method

The main advantage of cash accounting is its simplicity. You can manage a cash accounting system in a basic spreadsheet, which is helpful if your nonprofit isn’t ready to invest in specialized accounting software yet. It’s also relatively easy to understand no matter how much accounting knowledge you have since you’re just recording cash transactions as they take place.

However, there are several notable disadvantages to cash accounting, including that:

- It doesn’t comply with nonprofit financial reporting requirements, meaning you have to include special disclaimers on your tax returns.

- It’s less useful for future planning and goal-setting since you don’t have official, complete records of expected revenue or outstanding payments.

- It doesn’t include tracking for accounts receivable, accounts payable, and long-term assets, which tend to become more important as your organization grows.

It’s possible to solve this last problem by using a modified cash accounting system, in which you add additional sections to your spreadsheet to log assets, payables, and receivables. However, you still need to include reporting disclaimers if you do this.

Accrual Accounting Method

Mid-sized and large organizations tend to use the accrual accounting method to manage their complex financial situations more effectively. It’s slightly more complicated than cash accounting, but it’s straightforward enough once you understand how it works.

How It Works

Accrual accounting systems recognize revenue when it’s pledged and expenses when they’re incurred. Rather than monitoring cash flow, the purpose of accrual accounting is to track your nonprofit’s financial commitments—whether you’ve committed to paying an external party or a donor has committed to providing funding to your organization.

Returning to the earlier bikeathon example, if your organization used an accrual accounting system, you’d record the full cost of the supply rental (both the deposit and the outstanding balance) under this year’s expenses since you already committed to pay the full amount. Then, you’d record any peer-to-peer donations pledged in December under this year’s revenue and those pledged from January to March under next year’s.

Benefits & Drawbacks of This Method

Most of the advantages and disadvantages of accrual accounting are exactly the opposite of those associated with cash accounting. If the main benefit of cash accounting is simplicity, the main drawback of accrual accounting is its complexity. You’ll almost certainly have to purchase specialized accounting software to manage this type of system, and working with a dedicated accountant may also be necessary if you don’t have much financial management experience.

However, many organizations find these investments worthwhile because of the benefits accrual accounting provides. Since this method complies with nonprofit financial reporting standards, you don’t have to include the disclaimer on your tax returns. More than that, you’ll be able to produce more accurate reports, increasing transparency with supporters and stakeholders about how your organization is using its funding.

Additionally, having an accrual accounting system puts your nonprofit in a better position to plan for—and achieve!—future growth. Double the Donation’s guide to nonprofit capacity building emphasizes the importance of a comprehensive, up-to-date strategic plan with clearly defined goals and metrics in guiding your organization’s expansion. Accrual accounting allows for more effective financial decision-making, which will help you define your growth goals and measure your progress toward them.

Should My Nonprofit Use Cash Accounting or Accrual Accounting?

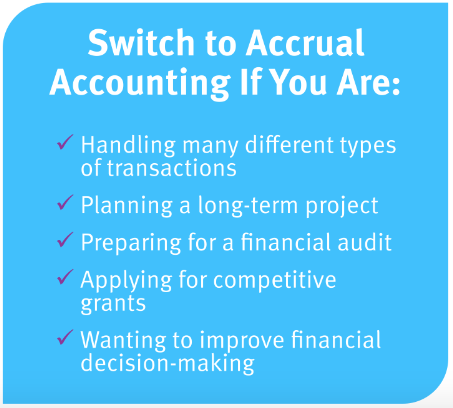

There is no one-size-fits-all approach to nonprofit accounting, so the answer to this question is it depends. Jitasa’s guide to cash vs. accrual accounting for nonprofits recommends using the accrual method if complex situations arise in your organization’s financial management, such as needing to:

There is no one-size-fits-all approach to nonprofit accounting, so the answer to this question is it depends. Jitasa’s guide to cash vs. accrual accounting for nonprofits recommends using the accrual method if complex situations arise in your organization’s financial management, such as needing to:

- Handle a larger volume and wider variety of transactions than you could feasibly track in a cash accounting system.

- Plan for a long-term project, such as a capital campaign.

- Prepare for a financial audit—that way, you can provide the auditor with comprehensive information to make helpful recommendations.

- Apply for competitive grants where the grantmakers will analyze applicants’ financial information carefully to make their decision.

- Improve your internal financial decision-making processes as you launch new initiatives.

However, if your organization is just getting started with accounting, the cash method is likely a good fit. Even if you don’t yet have the resources to invest in accounting software or professional help, you still need a unified system in place to track your nonprofit’s spending and fundraising. Plus, you can always add the modifications for assets, payables, and receivables if they become part of your financial situation before you’re ready to fully switch to the accrual method.

No matter which accounting method your organization uses, remember that the ultimate goal of nonprofit financial management is to further your mission. Your records—whether based on cash flow or financial commitments—should inform your decisions about operating your organization, fundraising, and delivering services to make a difference in your community.

Jon Osterburg has spent the last nine years helping more than 100 nonprofits around the world with their finances as a leader at Jitasa, an accounting firm that offers bookkeeping and accounting services to not-for-profit organizations.

Jon Osterburg has spent the last nine years helping more than 100 nonprofits around the world with their finances as a leader at Jitasa, an accounting firm that offers bookkeeping and accounting services to not-for-profit organizations.

I can’t wait to meet with you personally.

I can’t wait to meet with you personally.

Comments on this entry are closed.